Home

Feature

Oil Prices Hover Over World Economy and Farmers

Poster in Mar 15, 2022 21:48:46

Oil Prices Hover Over World Economy and Farmers

In the US, all eyes are on the cost of inputs. Inflation and increased energy costs were both factors well before Russia invaded Ukraine, and both have been exacerbated by the conflict. Just this week, inflation hit a new record high at 7.9%, and fuel—even red diesel for farm operations—is reaching all time highs. There was cautious optimism only weeks ago that the US long grain rice crop might be able to hold planted acres steady with last year, but that hope is quickly dwindling as input costs rise faster than anytime in recent history. It would not be a stretch to assert that the US long grain crop will drop by another 15% this year. In 2020, planted acres were 2.96 million acres. Last year in 2021, planted acres dropped 17% down to 2.53 million acres. This year, one can expect another 15% decrease, down to 2.15 million acres. This helps explain why long grain prices have found firm-footing despite lagging milled rice exports.

Paddy exports have been strong, which is the norm, but domestic milled business has been the true shining star this year. Milled exports to Haiti have leveled back out after the country imploded months ago and has generated steady millings. Iraq would be a saving grace, but right now the domestic business coupled with a short crop and drought in South America provides enough support to keep prices firm across all growing regions, and even provide some support for new crop pricing, despite it not being in the ground yet.

In South America, Brazil is particularly impacted by the Russia/Ukraine conflict. Brazil imports over 80% of its total fertilizer needs, and almost 100% of its nitrogen fertilizer from Russia. To circumvent the obvious concern and ensure fertilizer supplies for coming crop cycles, the Brazilian government has announced an emergency National Fertilizer Plan in which they intend to be able to produce 40% of their own fertilizers by the year 2050. The problem is, Brazil only produces about 4% of their own nitrogen-based fertilizers currently. This concern is obviously compounded by the drought, and creates an expectation that the harvest of their soybean, corn, sugar, and rice crops will be lighter both in acreage and in yields. This is one more reason that US farmers will cycle out of rice and into soybeans; China’s demand for soybeans doesn’t fade with the acres reduced by drought or yield reduced by unavailable fertilizer.

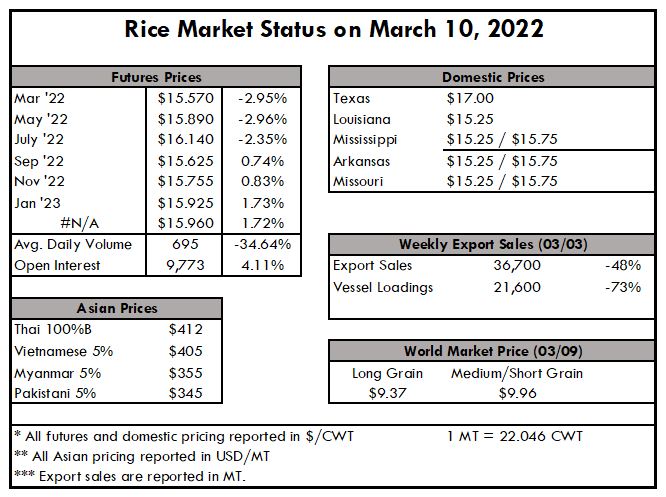

In Asia, Thai prices bumped to over $410pmt this week, again on the fluctuation of the Bhat. In the last three months, Thai prices have increased by 7%. Viet prices are holding steady just over $400 pmt, and in the last three months have fluctuated less than 5%. India and Pakistan tell the same story, only at lower price points around $360 pmt for the past three months and into the current cycle.

The weekly USDA Export Sales report shows Net sales this week of 36,700 MT were down 48% from the previous week and 61% from the prior 4-week average. Increases primarily for Mexico (14,700 MT), Japan (13,300 MT), Nicaragua (5,400 MT), Canada (2,500 MT), and Guatemala (1,500 MT), were offset by reductions for Costa Rica (1,500 MT). Exports of 21,600 MT were down 73% from the previous week and 74% from the prior 4-week average. The destinations were primarily to Haiti (15,300 MT), Canada (3,200 MT), Mexico (2,000 MT), Taiwan (300 MT), and Hong Kong (200 MT).

Comment Now